Campaigns

Latest News

-

Super on paid parental leave is a super win for women workers

07 March 2024 -

Media Statement: O’Dwyer ducks the big issue in women’s statement

20 November 2018 -

Media Statement: Government must fix super inequality

09 September 2018 -

Qantas mega-profits trickle up... not down

14 February 2018 -

Tell the Banking Royal Commission your story – counteract gag orders by Banks on staff and clients

09 February 2018

Superannuation & retirement

Stand up for Super

All Australians deserve a decent retirement

Australia’s universal superannuation system is the difference between poverty and a decent retirement for most Australians. Superannuation and the decisions that are made today will have a far-reaching impact on what retirement looks like for all hard-working Australians:

- It is the difference between using the heater during winter and having to shiver under a blanket.

- It is the difference between a healthy balanced diet or instant noodles for dinner.

- It is often the difference between being able to afford vital medications or not.

Australian families are worried about their future.

Just one in five Australians with superannuation said they expected to be able to live comfortably off their super in retirement. Many Australian women are retiring in poverty; older women are the fastest-growing cohort of people experiencing homelessness in Australia today.

What we want:

We want our elected representatives to stand up for super, to stand up and ensure every working Australian has a decent retirement. This means:

- Protecting our universal superannuation system and rejecting any attempts to make super optional for Australian workers

- Legislating to ensure superannuation is paid on every dollar earned by eliminating the $450 minimum threshold for compulsory employer contributions

- Keeping to the promised Superannuation Contribution Guarantee rate increase to 12%

- Closing the retirement gender super gap by paying a superannuation contribution at the prevailing SGC rate for the government’s paid parental leave scheme and on all government carer & family payments

Image: Stand Up For Super rally - Canberra Feb 2020

In October 2015 the ASU began a major project investigating women, super and retirement in great detail. Initially it was to write a submission for a Senate Inquiry into women's financial security in retirement, but as we delved further it became apparent that this area is in great need to work.

In July 2017, we partnered with progressive think tank Per Capita to release a comprehensive report and recommendations based on the investigations we did. Read about it and download the report here: Per Capita report reveals retirement is not so super for women

Women and low paid workers, many despite a lifetime of work, are retiring with minimal super and facing an uncertain future.

On average, women are retiring with almost half the super of men[1].

Why are women retiring with less?

- 67.9% of part-time workers are women

- Women working full-time earn 14% less than men

- Women take on average five years out of the workforce to care for children or family members – during which time they are not earning super

- An estimated 220,000 women miss out on $125 million of superannuation contributions as they do not meet the requirement to earn $450 per month (before tax) from one employer (as many women work more than one part-time job) [2]

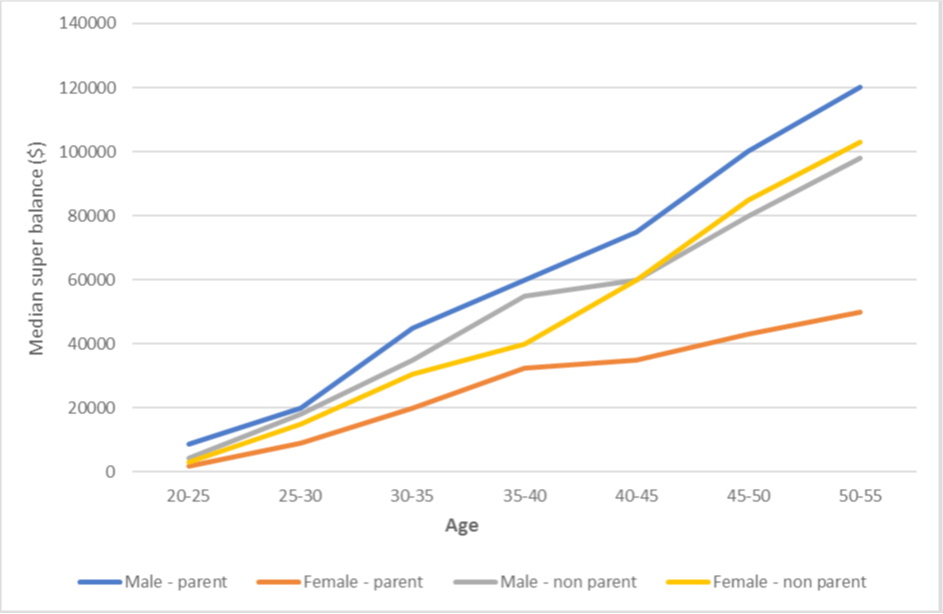

Figure: Median superannuation balances - parents and non-parents by age bracket. (Per Capita, 2017)

We need to take action to stamp out the retirement gender pay gap in retirement savings. This can be done by:

- Eliminating the $450 minimum threshold to enable over 1 million Australians to start saving for their retirement, over half of those women;

- Paying a superannuation contribution at the prevailing SGC rate for the government’s paid parental leave scheme and on any carer or family payments.

- Keeping to the legislated increase to the superannuation contribution guarantee to 12%.

Our universal superannuation system must work for all Australians to ensure everyone has a decent retirement and no woman retires in poverty.

[1] ASFA Superannuation account balances by age and gender report, October 2017.

[2] Who’s missing out on super? Wage threshold creates an underclass of biggest losers.